The first quarter of 2026 confirms an active foreign market in terms of volume, with around 24,800 sales and a 13.92% share of the national total (178,096 residential property transactions).

Beyond the stability of the figures, what is significant is the internal movement within the international market. Demand is not declining, but rather changing in composition and origin, which redefines the quarter.

A large proportion of the transactions completed during this period do not stem from recent decisions, but from processes initiated between 2024 and 2025, against a backdrop marked by regulatory changes, increased international tax pressure and a gradual adjustment of return expectations.

The New Map of Nationalities: less inertia, more selectivity

The first quarter does not mark a break in the market, but it does confirm clear shifts in its internal composition. Foreign buyers maintain their presence, albeit with a different structure to previous years.

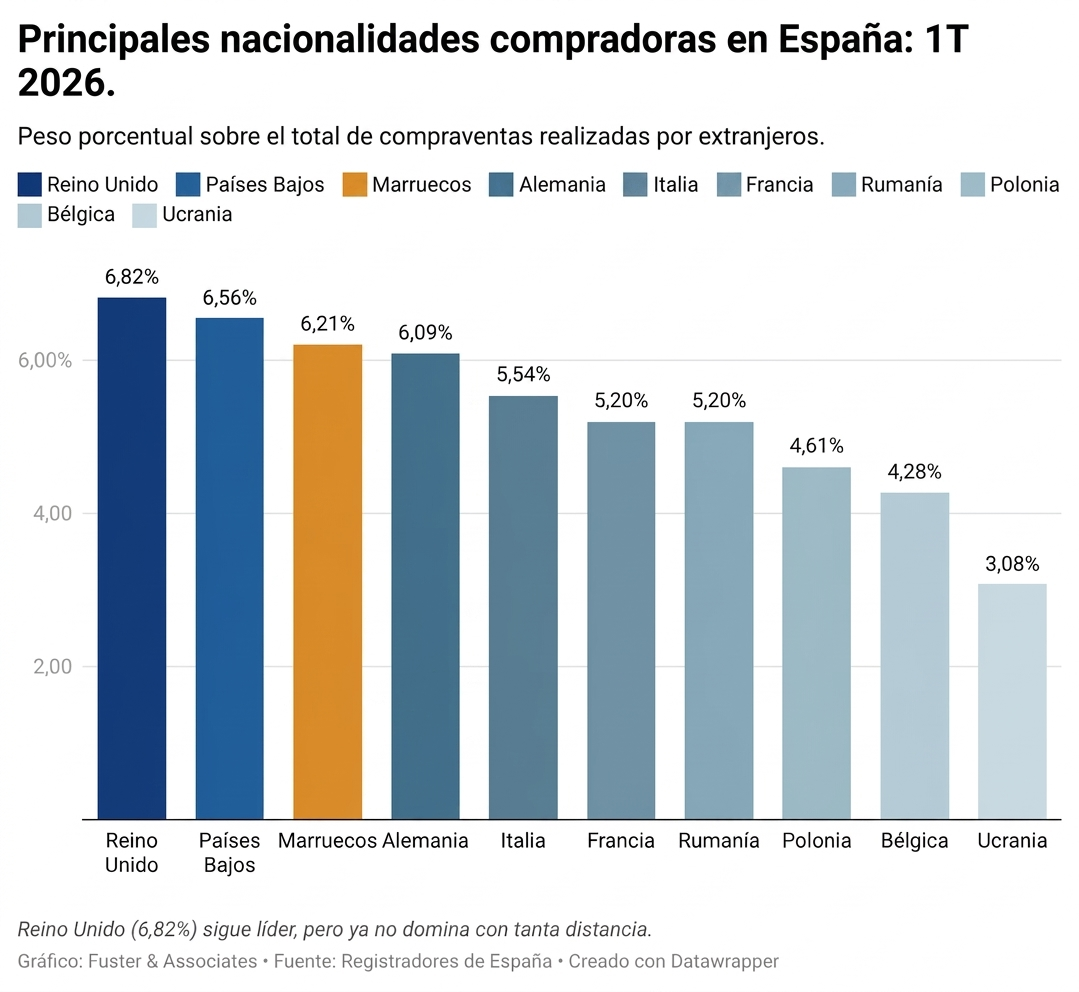

British: 7.93% → 6.82% (-1.11 pp)

1,668 sales.

A moderate adjustment is observed within a segment which, following the post-Brexit cycle, is losing some relative weight without this leading to a sharp drop in activity.

Dutch: 6.77% → 6.56% (-0.21 pp)

1,604 sales

They remain at levels very similar to those of the previous period, with stable performance within the European market.

Moroccans: 5.75% → 6.21% (+0.46 pp)

1,518 sales.

Strengthening of the residential component compared to purely investment-driven activity.

Germans: 6.65% → 6.09% (-0.56 pp)

1,489 sales.

Stable profile, with greater sensitivity to legal certainty and the efficiency of the purchasing process.

Geography: The Mediterranean Arc is consolidating as a system, not as a market

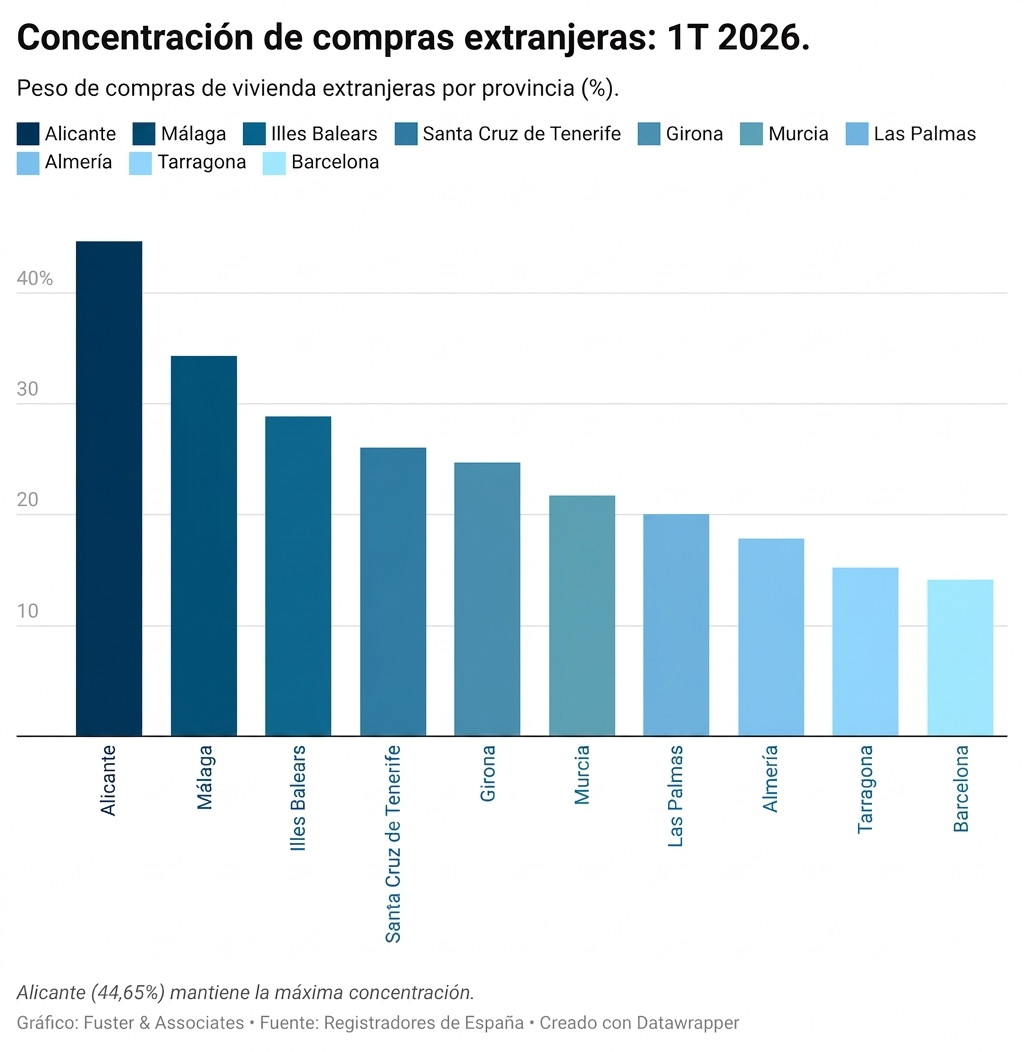

The territorial distribution reinforces an increasingly clear picture: the foreign buyer no longer behaves as if choosing between provinces, but between micro-markets with their own dynamics within the Mediterranean Arc.

In Alicante, where foreign buyers account for 44.65%, the market is at a critical juncture. Price levels raise the entry threshold and shift the decision-making process towards a more technical approach, typically preceded by a very thorough assessment of the property.

The Region of Murcia, with 21.73%, is establishing itself as a structural alternative. It competes not only on price, but also on the perception of accessibility: a market seen as a more controlled entry point within the Mediterranean coastline.

Almería, with 17.84%, continues to expand, driven by new-build developments and a product increasingly geared towards foreign demand, which is redefining its position within the wider market.

In Málaga, where 34.30% of sales are driven by international demand, the market is establishing itself as one of the main centres of attraction in southern Europe. The intensity of demand is not only holding steady but is reinforcing its structural nature.

Valencia, with 13.05%, shows a more mixed picture. Foreign buyers coexist with profiles driven by work mobility, part-time residence and less uniform decision-making, which dilutes the strictly investment-driven interpretation seen in the rest of the Arc.

Price: the market is no longer homogeneous

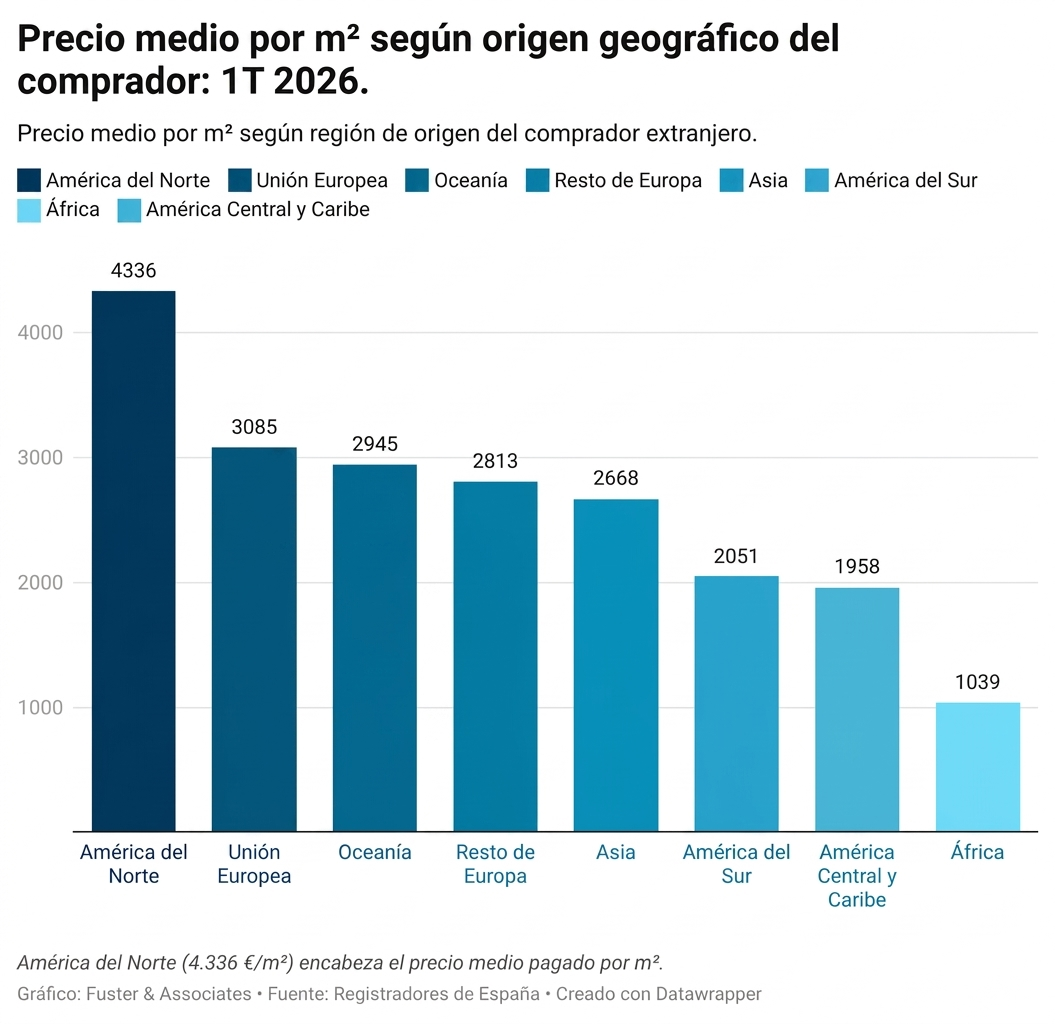

The average price per square metre confirms an already structural dynamic: Spain functions as a fragmented market. The gap between prime areas and secondary markets is widening not only in terms of price but also in the profile of the buyer accessing each segment.

In this context, buyers from North America and the European Union are situated at the highest price levels. Not because they pay more for comparable assets, but due to a clear concentration on locations with higher perceived quality, greater regulatory stability and less friction in the acquisition process.

New-Build vs Second-Hand Housing: two speeds that are already shaping the market

The first-quarter report confirms divergent trends between new-build and second-hand housing, which can no longer be interpreted as a one-off phenomenon, but as a structural pattern.

New-build housing recorded growth of 7.2%, whilst second-hand housing fell by 2.0%.

The growth in new-build housing is partly due to developments marketed in 2023 and 2024, which are now entering the deed registration phase and appearing in the registrars’ statistics.

At the same time, the existing housing market is losing momentum in the foreign market. This adjustment is not due to a lack of demand, but rather to increased selectivity: opportunistic buying is declining, and decisions are focusing on properties with greater perceived viability, established locations, or price levels that offset exposure to regulatory uncertainty.

The result is a market operating at two speeds, with new-builds acting as a continuation of previous decisions and the second-hand housing market serving as a more immediate barometer of the selective tightening of demand

The Silent Factor: regulation, taxation & shifting expectations

Between 2024 and 2025, a series of factors took hold that now explain much of the behaviour of the international market in Spain. They do not act as immediate shocks, but rather as a cumulative decision-making environment.

These include progressive restrictions on tourist rentals in certain areas, the review of tax incentives in source countries, a more challenging interest rate environment and increased macroeconomic uncertainty in cross-border investment.

These are not sudden changes, but shifts in the perception of risk. And the first quarter of 2026 reflects this adjustment in expectations with a lag.

“Today, buyers no longer buy into stories; they buy into validation,” notes Pedro Martínez, CEO of Fuster & Associates. “Interest in Spain is not waning, but the entry point has changed. The decision is driven less by emotion and more by technical verification of the asset.”

A Market Slower To Decide, Quicker To Rule Out

The first quarter of 2026 does not reflect a loss of momentum, but rather a change in the way international buyers operate.

They maintain their investment capacity, but introduce more filters in the early stages of the process. This reduces impulsive buying, increases preliminary analysis and shifts part of the risk to stages prior to the formal decision.

In this context, the closing of a deal depends less and less on initial interest and more on the soundness of the prior legal and tax due diligence.

The difference between a transaction that goes through and one that falls through is determined before the reservation. And this shift is now structural.

At Fuster & Associates, with over 25 years’ experience in providing legal and tax advice to foreign buyers in Spain, we operate in the main hubs of demand across the Mediterranean region, with offices in Valencia city centre, Alicante (La Zenia, Teulada and Finestrat), Murcia (Los Alcázares and the city centre) and Almería (San Juan de los Terreros – Pulpí).

Our multicultural team, fluent in over a dozen languages, works within a context where market changes are not interpreted as isolated phenomena, but as direct responses to developments in the regulatory and tax environment.

Within this framework, the focus is on anticipating legal and tax issues before they affect the transaction, reducing uncertainty in the early stages and ensuring that transactions proceed to the notary without significant setbacks.